MSI Is A Global Association Of Over 250 Independent Legal And Accounting Firms In More Than 100 Countries. MSI Has A Successful Track Record Of More Than 25 Years And The Firm Has Recently Been Selected To Represent Mumbai, India.

Please Click Here To See MSI’s Info Graphic Which Highlights Key Facts Of The About. With The Membership At MSI, The Firm Has Now Access To 253 Legal And Accounting Firms Worldwide For Its Clients Who Desire To Do Cross Border Transactions Across The World.

REIT REGIME IN INDIA

- NTRODUCTION

The draft SEBI (Real Estate Investment Trusts) Regulations, 2013 (“REIT Regulations”) is yet another attempt of Securities Exchange Board of India (“SEBI”) to bring about the Real Estate Investment Trusts (“REIT”) regime in India. SEBI, in 2007, released the first draft of the REIT Regulations. Thereafter in 2008, SEBI introduced REITS via a new investment vehicle Real Estate Mutual Funds (“REMFs”) under the SEBI (Mutual Fund) Regulations, 1996 which did not see much success due to various tax and other issues. This update is our endeavor to provide you with our analyses of the key provisions of the REIT Regulations and challenges in implementation thereof.

- NEED

Indian real estate market has seen a rapid growth and has the potential of growing much further. To this end, REIT will help the real estate industry by providing an exit to the sponsor which will provide them liquidity and the ability to invest in other projects and on the other hand the investors will get an avenue where they can earn regularly by investing in ‘complete’ properties which are less riskier than the ‘under construction’ properties.

- BROAD FRAMEWORK

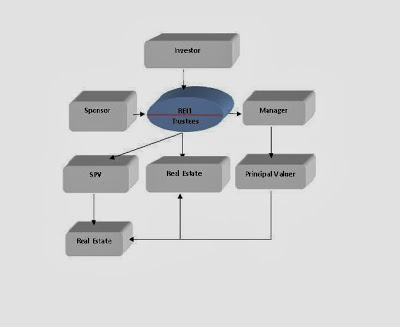

- Sponsor(s) to set up trust under the provisions of Indian Trust Act, 1882 and appoint trustee. Trustee shall enter into investment management agreement with the manager on behalf of the trust. Manager to appoint principal valuer, any other valuers, auditor, registrar and transfer agent, merchant banker, custodian and any other intermediary/ service provider required.

- Trust to apply for registration with SEBI as REIT as per the procedure laid down under REIT Regulations. Manager to identify and recommend investment opportunities for investment by REIT. After due diligence by the Trustee, the REIT, either directly or through a Special Purpose Vehicle, to invest in the real estate assets which shall be held by the Trustee in the name of REIT for the benefit of unit holders. However, sponsor to hold 25% or more of the total units of the REIT prior to initial offer.

- After registration of REIT and full valuation of REIT assets by principal valuer, if REIT holds RE assets of the value of more than INR 10 billion, 25% or more of the units of the RE assets maybe offered to public via initial offer as per the procedure laid down under REIT Regulations.

- Units of REITS to be listed within 15 days of closure of the initial offer. Once the units are listed and full valuation of all REIT assets has been done by the principal valuer, follow on offers can be made to the public.

- Sponsor to maintain 25% stake in REIT assets for 3 years from the date of listing of the units.

- Declaration of dividends as per the offer document/ follow-on offer document by the manger.

- Manager to distribute not less than 90% of the net distributable income after tax of the REIT to the unit holders as dividends.

- PARTIES TO THE REIT STRUCTURE

The REIT Regulations prescribe the eligibility criterion, the roles and responsibilities and tenure of the each of the parties involved in the REIT structure. REIT structure has the following parties:

-

- Sponsor(s): Net worth on consolidated basis to be INR 200 million and industry experience of 5 years on individual basis. They can exit REIT after 3 years from listing of the units by selling their stake (which has to be 15% at all times) to re-designated sponsors after obtaining approval from the unit holders.

- Trustee: Has to be registered with SEBI under SEBI (Debenture Trustee) Regulations, 1993. Should not be an associate of the sponsor/ manager/ principal valuer. 50% or more of its directors to be independent and not related parties to REIT.

- Manager: Net worth to be INR 50 million or more. Further, the manager and 2 or more key personnel in its Investment Committee to have 5 or more year experience in fund management/ advisory services/ property management in real estate industry or in development of real estate . More than half of the members of the Investment Committee to be independent. Manager may be removed with the approval of the unit holders.

- Principal Valuer: Principal valuer should have 5 or more years of experience in valuation of real estate. Should not be an associate of sponsor/ manager/ trustee. Principal valuer may be removed with the approval of the unit holders. Must be changed in every 2 years.

- Re-designated sponsor: Sponser(s) will arrange for them after obtaining the approval of the unit holders. Same requirements as sponsor.

- RESTRICTIONS

- Investment can only be in securities and real estate in India.

- Investment cannot be vacant or agricultural land or mortgages other than mortgage backed with security.

- 90% of the value of REIT assets to be invested in completed and rent generating properties. Completed properties are properties which have received occupancy certificates and rent generating properties are properties of which 75% or more area has been rented/ leased out.

- Only 10% of the value of REIT assets to be invested in developmental properties, listed or unlisted debt of companies, mortgage backed securities, government securities etc.

- Investment in developmental properties by REITs has to be locked in for 3 years after completion and should be leased out.

- 75% or more gains made by REITs excluding the gains made by disposal of properties shall be from rental, leasing and letting real estate assets.

- Investors to subscribe to a minimum of 2 units in REIT. Each unit of REIT to be of INR 0.1 million.

- Unit holders can only sell their units on the stock exchange.

- VALUATIONS, DISCLOSURES, AUDIT AND DELISTING

- The manager to ensure that Net Asset Value of REIT is calculated once in every 6 months by principal valuer and declared to the stock exchange.

- The principal valuer to conduct full valuation of REIT once in a year including physical inspection.

- REITs have to make several disclosures under the REIT Regulations. The trustee to oversee that the manager ensures that the disclosures/ reporting to the unit holders, SEBI, trustees and recognized stock exchanges are adequate, timely and in accordance with the REIT Regulations.

- The manager to ensure that the audit of accounts of REIT by auditor is done at least twice in a year and the report is submitted to the exchanges within 45 days of end of such half year.

- Delisting of the REIT units to take place in the events of following: Minimum public float falls below the prescribed 25%; or Number of unit holders fall below 20 (excluding related parties); or SEBI or stock exchange require delisting for (a) violation of the listing agreement or (b) in the interest of unit holders; or Sponsor/ manager request delisting with the approval of requisite unit holders; or Unit holders apply for delisting.

- CONCERNS

REIT Regulations while drafted carefully raise concerns on tax, stamp duty, distribution of income, foreign praticpation etc. We have discussed a few significant issues below:

- Tax issues: If a Sponsor transfers the real estate asset to Trust (on behalf of REITs), it will attract capital gains under the Indian Income Tax Act, 1961 (“Income Tax Act”). Please note that the Sponsor will not be able to transfer the property at a nominal value as the ready reckoner value will be the sale price. We recommend that capital gains on such transfer should be waived as it not actual transfer but transfer from one promoter entity to another.

- Stamp Duty: Transfer of real estate from the Sponsor to the Trust (on behalf of REITs) will attract stamp duty for conveyance. In most of the urban cities, conveyance would attract a stamp duty of 5% of market value or actual value of the sale. This will substantially increase the cost and may make REIT unattractive for the real estate companies. We recommend some concession on the stamp duty should be granted to promote REIT.

- Distribution of Income: The framework requires distribution of dividend as per offer document. If REIT holds shares of SPV, any distribution of profits will be subject to a corporate tax of 30% on SPV and dividend distribution tax of 15%. We recommend that such SPV under the REITs should be exempted from corporate tax, dividend distribution tax and Minimum Alternate Tax and should be given pass through status similar to venture capital funds provided Section 10(23FB) if the Income Tax Act providing single level of tax in the hands of the unit holders.

- Title of Property: REIT Regulations require the Trustee to ensure that the real estate asset has a proper legal and marketable title and all material contracts entered into by REIT are binding and enforceable. We believe that most of the immovable properties in India have some minor issues with respect to verify the title and hence the title should restrict to marketability of real estate. Further, such liability should be of the Sponsor who will transfer the property to REITs and not that of the Trustees.

- Limited Liability Partnership (“LLP”): After 2008, LLP has been the flavour for developers to hold the real estate asset. We recommend that definition of SPV and body corporate in the REIT Regulation should include LLP thereby enabling Sponsors more flexibility in their investments.

- Foreign Investment: REIT Regulations permit foreign investors to invest in REITs subject to exchange control regulations. Reserve Bank of India will be required to liberalise current regulations to specifically allow REIT investments by non-residents as direct investment is presently restricted in real estate business subject to conditions and investment in Trust requires approval of Foreign Investment Promotion Board.

- Units of REITs to qualify as security: Units of REITs should be defined as ‘security’ under Securities Control Regulation Act, 1956 , as these need to be compulsorily listed under the REIT Regulations

MHCO COMMENTS

If majority concerns raised by the industry are addressed by SEBI, REIT could evolve as a preferred mode of investment for the investors. Further, it will provide liquidity and transparency to the much required real estate sector. With the recent trend of Indian companies to list their real estate in Singapore exchange, REITs will boost the Indian real estate market.

The information contained in this communication is intended solely for the use of the individual or entity to whom it is addressed and others authorized to receive it. This communication may contain confidential or legally privileged information. If you are not the intended recipient, any disclosure, copying, distribution or action taken relying on the contents is prohibited and may be unlawful. If you have received this communication in error, or if you or your employer does not consent to email messages of this kind, please notify the sender immediately by responding to this email and then delete it from your system. No liability is accepted for any harm that may be caused to your systems or data by this message.

OUR CLIENTS

MEDIA COVERAGES

AWARDS & RECOGNITION

AFFILIATIONS & ASSOCIATIONS

MEMBERS OF MSI GLOBAL ALLIANCE

MEMBERS OF ILF

International Law Firms (ILF) Is An International Association Of Independent Smaller And Mid-Sized Law Firms Serving Their Clients’ Needs In Cross Border Business Legal Issues. Our Association With ILF Enables Us To Effectively Assist Clients With Trans-National Legal Issues At Effective Prices.

LIFE AT MHCO

PRACTICE AREA

Private Limited Company Registration in India

Setting up a Company in India

Foreign Direct Investment (FDI) in India

Foreign Business Registration in India

Small Business Registration in India

GET IN TOUCH

Mumbai: Surya Mahal, 2nd Floor 5, Burjorji Bharcha Marg Fort, Mumbai-400 023 India

Contact No.: T: +91-22-40565252

E: contact@mhcolaw.com

Delhi: C-9, Lower Ground Floor Jangpura Extension, New Delhi-110 0014 India

Contact No.: T: +91-11-40196496

E: contact@mhcolaw.com

Contact No.: T: +91-22-40565252

E: contact@mhcolaw.com

Delhi: C-9, Lower Ground Floor Jangpura Extension, New Delhi-110 0014 India

Contact No.: T: +91-11-40196496

E: contact@mhcolaw.com

2025 - MANSUKHLAL HIRALAL & CO.

Need Help? Chat with us